What Is Insurance Redlining?

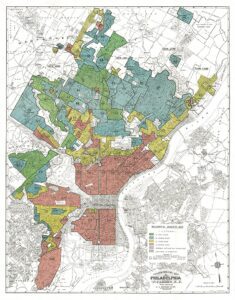

“Redlining,” in the insurance context, is an illegal practice in which insurance companies avoid providing insurance to individuals living in communities because of the race, color, or national origin of the residents in those communities. Redlining refers to the actual red patches that appeared on color-coded maps that were used to determine which neighborhoods were considered safer or riskier bets for home loans. Areas in red — usually neighborhoods with majority black populations — were deemed the biggest risks, and therefore, people within them were consistently denied home loans and other services. The Civil Rights Movement prompted “anti-redlining” laws that still impact insurance today.

How Was Redlining Used?

While today the process of redlining usually refers to any race-based segregation and discrimination tactics in real estate, the specific term “redlining” had its origins in government homeownership programs that were created as part of the New Deal in the 1930s. According to Wikipedia:

“[Redlining] had its origins in sales practices of the National Association of Real Estate Boards and theories about race and property values codified by economists surrounding Richard T. Ely and his Institute for Research in Land Economics and Public Utilities, founded at the University of Wisconsin in 1920. With the National Housing Act of 1934 the federal government began to be involved in the practice and the concurrent establishment of the Federal Housing Administration (FHA). The FHA’s formalized redlining process was developed by their Chief Land Economist, Homer Hoyt, as part of an initiative to develop the first underwriting criteria for mortgages.

The same Wikipedia article goes on to state that redlining was reinforced by private organizations and federal policies in the mid-20th century. The FHA’s appraisal manuals directed banks to avoid areas with racially diverse populations and suggested cities implement racially restrictive zoning laws. Consequently, between 1945 and 1959, African Americans received less than 2% of all federally insured home loans, highlighting the extent of racial discrimination in housing finance. [1]

What Is an Example of Insurance Redlining?

A law review article published last year, “The Color of Property and Auto Insurance: Time for Change,” set forth a historical issue of race discrimination in the property insurance market with the following example of it against a future black Supreme Court Justice:

Thurgood Marshall was denied auto insurance when he lived in Harlem in 1940 because, he was told, it was a ‘congested area.’ He wrote that although the problem of insurance discrimination was getting worse, it was ‘practically impossible to work out a court case because the insurance is usually refused on some technical ground.’ [2]

While redlining originally referred specifically to the practice of denying home loans in non-white neighborhoods, loans are just one of many financial products that were consistently harder to access in areas deemed too “risky.” Not only banks and mortgage lenders, but also property insurance companies, adopted strict redlining policies after World War II:

According to urban historian Bench Ansfield, the postwar advent of comprehensive homeowners’ insurance was limited to the suburbs and withheld from neighborhoods of color in U.S. cities. One Aetna bulletin from 1964 advised underwriters to ‘use a red line around questionable areas on territorial maps.’ The New York Urban Coalition warned in 1978, ‘A neighborhood without insurance is a neighborhood doomed to death.’

The History of Insurance Redlining

That same law review article noted the long history of racial discrimination in property insurance that led to laws preventing those practices today. African Americans were often excluded from homeownership due to practices by insurance companies and the federal government. The Hughes Report revealed that even before the urban riots of the 1960s, adequate insurance was scarce in these areas. This issue extended to reinsurance, as companies struggled to obtain it for urban areas at reasonable prices.

The article goes further to show that the financial structure of the insurance industry favored practices that discouraged insuring African American neighborhoods. It describes how the Hughes Report further uncovered that insurance companies’ decisions to avoid urban areas or charge more were not based on solid data but on unfounded assumptions about costs and risks.

The Civil Rights Movement, led by Martin Luther King Jr., resulted in laws impacting property insurance and its availability. While there have been many reforms since then, laws are rarely perfect. The issues of racial discrimination in the property insurance market are still being studied today, with new laws addressing novel methods of such discrimination.

Insurance Redlining Today

Despite laws attempting to address this inequity, issues of “redlining” and racial discrimination still exist in the property insurance market. In his work, Towards A Civil Rights Approach to Insurance Anti-Discrimination Law, Professor Daniel Schwarcz noted the following:

Despite the significance of insurance discrimination in modern America, the law does remarkably little to police against the risk that this discrimination will unfairly harm minority or low-income communities. [3]

Schwarcz goes on to discuss the inadequacy of current laws in addressing insurance discrimination in the United States, particularly against minority or low-income communities. State laws against ‘unfair discrimination’ in property and casualty insurance require only that insurers justify their discriminatory practices actuarially. Although some states forbid discrimination based on race, ethnicity, national origin, or income, these laws are interpreted very narrowly, effectively only preventing insurers from explicitly including these characteristics in their models or deliberately using proxies for them. [3]

Looking For More Resources?

If you’re looking for more information about how to protect yourself as a homeowner, visit Merlin Law’s resource library to read about how others have successfully navigated legal issues that arise around insurance claims:

- Fighting Against Insurer Tactics

- Fighting for the Underdog

- What to do When You Have a Denied or Underpaid Claim

2 Daniel Schwarcz, Towards A Civil Rights Approach to Insurance Anti-Discrimination Law, 69 DEPAUL L. REV. 657 (2020), available at https://scholarship.law.umn.edu/faculty_articles/697.