Bill Wilson has a commentary about insurance, which is widely read. For all of my insurance coverage nerds who love policy language, his blog and book are must reads. I made this same point six years ago in Insurance Commentary with Bill Wilson is a Good Insurance Coverage Read. It is still true today.

In a post you should read following mine, One of the Most Frustrating Claims of My Career, he made the following commentary:

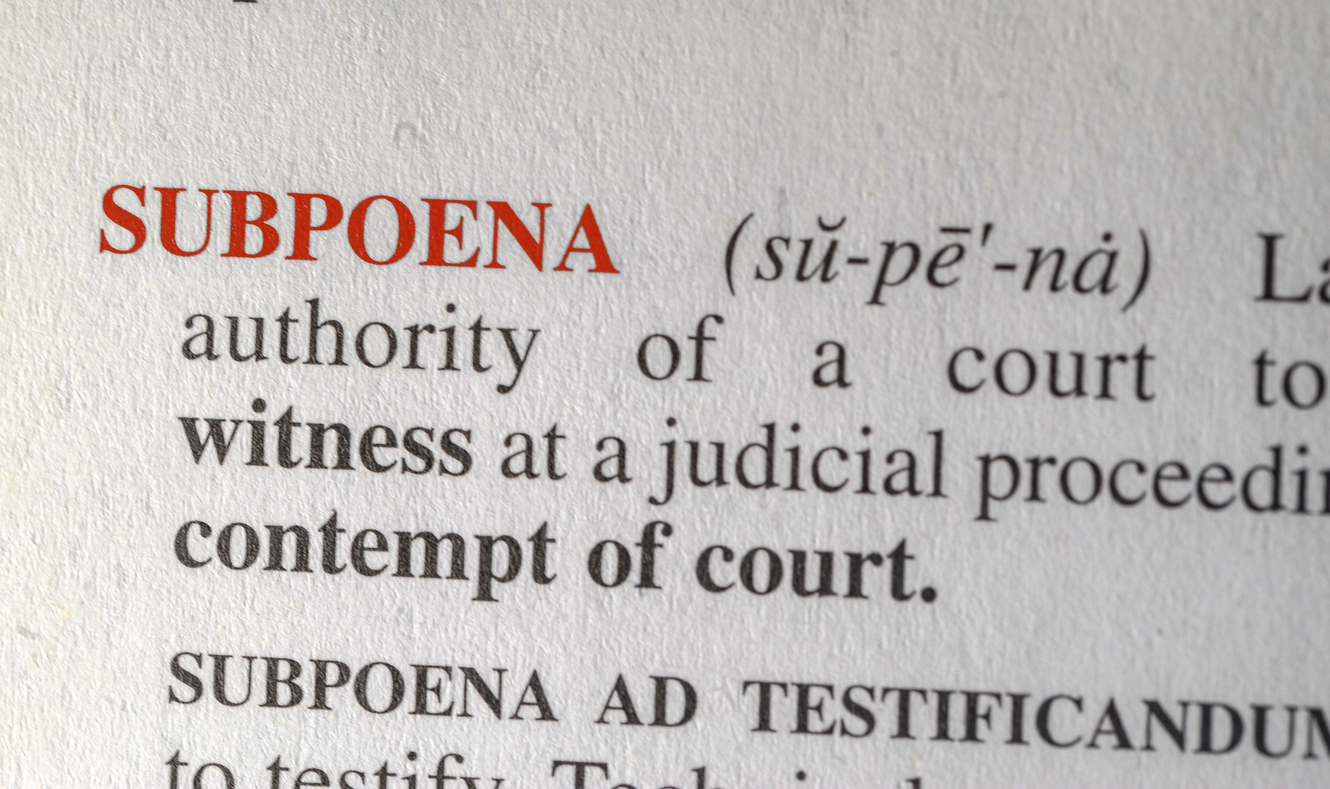

Theft is also defined statutorily in many, or most, states. For example, here’s a typical definition: ‘A person commits theft of property if, with intent to deprive the owner of property, the person knowingly obtains or exercises control over the property without the owner’s effective consent.’

Could it be any clearer? Theft includes fraud, swindling, deception, etc. In fact, even if someone ‘obtains possession of property by lawful means and thereafter appropriates the property to the taker’s own use’ (e.g., conversion), they have committed a theft. So, even if the ‘purchaser’ had given the insured a valid check and later stopped payment on it with the intent of depriving the insured of its possession, a theft has been committed.

The insurer’s reference to ‘voluntary parting’ is immaterial. Voluntary parting is a loss often excluded by commercial property and crime forms. For example, the CP 10 30 10 00 covers theft but has the following exclusion:

‘Voluntary parting with any property by you or anyone else to whom you have entrusted the property if induced to do so by any fraudulent scheme, trick, device or false pretense.’

That doesn’t mean that voluntary parting isn’t theft…what it means is that the form covers theft but not when the theft occurs through voluntary parting due to fraud, trick, etc. More important, that language does not appear in the HO forms.

We ran this claim by our faculty members and every single one of them said this was a theft…pure and simple. The position of the insurer that the insured no longer owns the ring and the claim is for a counterfeit check she now owns is a laughable premise (if this was a laughing matter). The insured’s loss is the ring, not the monetary funds represented by a counterfeit check (which is the purpose of that Additional Coverage). At the precise moment the insured exchanged the ring for a check known to be worthless by the other party, a theft occurred.

You will have to read the rest of the story by going to his blog. You should also note that the policyholder eventually had to seek an attorney.

The bottom-line lesson is that the more you read about how coverage applies, the better you become at helping policyholders obtain coverage. We read and study Bill Wilson at Merlin Law Group. So should you.

Thought For The Day

It’s not that I’m so smart, it’s just that I stay with problems longer.

—Albert Einstein