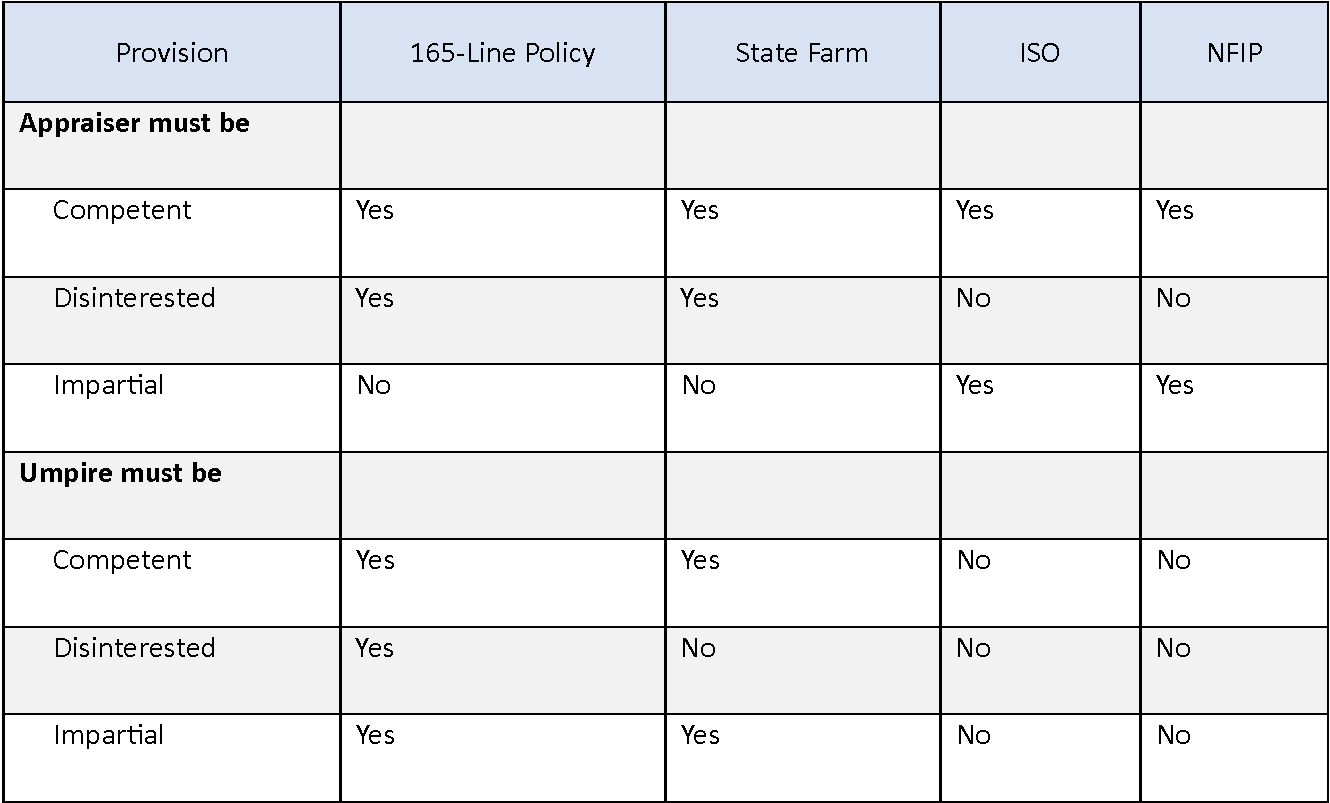

Four years ago, I posted Appraisal: Competent, Disinterested and Impartial. Are appraisers and Umpires Ever Actually Any of the Three?, and posted the following chart:

All the listed policies require the appraiser to be “competent.” What does that mean? How do you determine if a potential appraiser is competent?

The first rule to remember for participants in an appraisal proceeding is to determine what state law applies, as highlighted last week in Rhode Island Appraisals—The Arbitration Act Applies to Determine the Partiality of Appraisers and Umpires:

Should Appraisers Be Advocates For A Party To An Appraisal? noted the importance for insurance appraisal participants to first determine what state law applies. A clear example of this important point is the post, Appraisal Is Not Governed Under Arbitration Rules in Utah, where Utah directly holds that appraisal is not arbitration and the Utah Arbitration Act does not apply to an insurance appraisal. Contrary to that view, Rhode Island directly finds that its arbitration laws apply to insurance loss appraisals.

Last week, a New York court considered whether the policyholder’s appraiser could be competent because the appointed appraiser previously made a determination based on the value of the loss.1 The court addressed the factual situation as follows:

[T]he Court granted Defendant’s motion to compel appraisal and ordered each party to select an appraiser as outlined in the parties’ insurance policy. The policy requires ‘each party [to] select a competent and impartial appraiser and notify the other of the appraiser within 20 days of [the Court’s] order.’ Defendant selected Andrew T. Clark of Meaden & Moore and Plaintiffs selected David Zweighaft of RDZ Forensic Associates. Mr. Zweighaft is the forensic accountant who analyzed Plaintiffs’ books and records and prepared their original loss of business income claim.…

Defendant claims that Mr. Zweighaft is incapable of serving as a ‘competent and impartial appraiser’ because he prepared the original claim that is subject to challenge. As such, it has moved to appoint an appraiser pursuant to N.Y. CPLR § 7504. ECF No. 30. Plaintiffs oppose this relief on the grounds that Mr. Zweighaft’s prior analysis does not, as a matter of law, disqualify him as competent and impartial.

The court found that the policyholder’s appointed appraiser could continue in that capacity despite previously valuing and determining the amount of the policyholder’s loss:

The Court declines to find that Mr. Zweighaft’s role in this dispute disqualifies him as Plaintiffs’ selected appraiser. See generally 70A N.Y. Jur. 2d Insurance § 2272 (2023) (the ‘mere fact’ that an appraiser previously ‘made a computation of the loss[] does not, as a matter of law, disqualify such appraiser’).

On a side issue about whether an appraiser in New York can act as an advocate for a party to an appraisal, the policyholder’s brief cited an interesting older New York case which stated:

This is a motion to declare an appraiser disqualified on the ground that he is not disinterested. The motion is denied. There is no showing whatsoever that the appraiser in question has any financial or other interest which would disqualify him. It is to be noted that, under the terms of the very order providing for the appointment of appraisers, the appraisers designated by the respective parties are to be paid by said parties, so that the mere circumstance that the appraiser in question is to be paid by the respondent is not enough to disqualify him. Petitioner apparently relies upon his claim that the appraiser had urged that the insurer pay the amount which he had found to be the damage suffered. Statement that the appraiser ‘took charge of the claim’ and acted as ‘an advocate on behalf of Mr. Ducas’ are mere conclusory characterizations. All that actually appears to have happened is that the appraiser urged his estimate of the amount of the damages upon the insurance company. It is quite natural for an appraiser to attempt to vindicate his own findings and attempt to have others agree with him. His mere doing so is insufficient, in and of itself, to disqualify him on the ground that he is not a disinterested appraiser. For aught that appears in the papers the appraiser to be designated by the insurance company and paid by the latter cannot reasonably be expected to be any more disinterested than the appraiser now sought to be disqualified.2

The answer to today’s posted question is “It depends on state law.” In this case, a New York court allowed a party who was apparently being paid on an hourly basis to be an appointed appraiser, despite having determined the amount of the loss at issue before the appraisal was demanded. Always check with a reputable lawyer to get an opinion about the law if you are unsure what law should be followed.

Thought For The Day

You can get a million different opinions from different people, but I always like to watch myself to see what I did and how I performed because the best critic is yourself.

—Mandy Rose

1 Victor’s Café 52nd Street v. Travelers Ind. Co. of America, No. 22-cv-07223 (S.D. NY July 31, 2023).